INTRODUCTION

A Meeting in layman’s terms means when people come together to discuss something. Similarly there are various types of meetings defined under the Companies Act 2013.

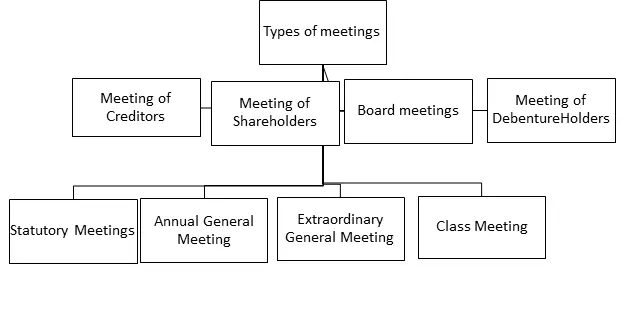

- Meeting of Creditors: These types of meetings are not exactly meeting of the company as creditors are usually outsiders. A meeting of creditors is organized by the company to formulate schemes or even in case of voluntary winding up. Section 391[1] of the Companies Act,2013 deals with the meeting of creditors

- Meeting of Shareholders: These meetings can be classified into four types namely:

- Statutory meeting: The first Annual General Meeting of a company is called a statutory meeting. It was a compulsory provision now it is discretionary.

- Annual General Meeting: As the name suggests this meeting is conducted once every year for all kinds of companies (private, Public etc.) except a one-person company. The requirements for this meeting is:

1. Annual general meeting should be held once in each calendar year.

2. First annual general meeting of the company should be held within 9 months from the closing of the first financial year. Hence it shall not be necessary for the company to hold any annual general meeting in the year of its incorporation.

3. Subsequent annual general meeting of the company should be held within 6 months from the date of closing of the relevant financial year.

4. The gap between two annual general meetings shall not exceed 15 months.

In case where an AGM is not possible the registrar may extend it up to 3 months. Both ordinary as well as special business is discussed in an AGM and the penalty for not conducting one lies in section 99[2] of the act.

- Extraordinary General Meeting: There are certain matters of the company which need to be discussed urgently and cannot wait till the next AGM. For this purpose, a provision for Extraordinary General Meeting (EOGM) exists in section 100[3].

An EGM can be called by:

- By the board (section 100(1))[4]

- By board on requisition of members (section 100(2))[5]

- By requisitionists(section 100(4))[6]

- By Tribunal (section 98)[7]

- Class Meeting: In these types of meeting only a particular class of shareholders attend and decide on issues which are only binding to their particular class. Other classes may not attend and vote in this type of a meeting. According to the section 92(1)(f) [8] details of such a meeting are to be published in the annual return.

- Board Meetings[9]: The meeting of directors are called board meetings and are especially important as the control of the company lies with the directors. They meet frequently to discuss the working of the company. These meetings must have a purpose, must be held with proper notice as well as have an effective chair. It must also be documented.[10]

- Meeting of debenture holders: A particular class of debenture holders conduct this type of meeting to discuss changes in their rights etc.

Conclusion

Thus, the 2013 act has comprehensively discussed the various types of meetings and the rules and regulations concerning them. As well as the procedure of calling a meeting and the responsibilities of the officers concerned.

[1] Section 391 of The Companies Act,2013.

[2] Section 99 of The Companies Act,2013.

[3] Section 100 of The Companies Act,2013.

[4] Section 100(1) of The Companies Act,2013.

[5] Section 100(2) of The Companies Act,2013.

[6] Section 100(4) of The Companies Act,2013.

[7] Section 98 of The Companies Act,2013.

[8] Section 92(1)(f) of The Companies Act,2013.

[9] Section 173 of The Companies Act,2013.

[10] Section 118 of The Companies Act,2013.